Gaps in health insurance plans are resulting in increasing allergy prevalence in India

Allergy is hypersensitivity of the immune system or abnormal reaction of the immune system to foreign antigens. Allergy-related common diseases include allergic rhinitis, urticaria, eczema, anaphylaxis, conjunctivitis, and asthma. Allergy may affect the lungs, stomach, skin, nose, throat, and eyes. However, various technologies and intervention methods have helped in reducing the negative impacts of allergy. The increasing allergy prevalence based diseases indicate the lack of medical care or service in India. 25% of the Indian population suffers from various forms of allergy, out of which 30% suffer from allergic rhinitis and 15% of from atopic asthma as in 2014.

However, these statistics for allergic rhinitis and atopic asthma has increased by approximately 5% in 2017. Medical insurance plays a major role in helping people to reduce the burden of instantaneous expenditure for hospitalization and treatment (Ilangovan, 2014). Moreover, the growth rate of private medical insurance is merely an average of 5% from 2012 through 2017. In India, more people are medically funded by the government. However, according to the report of National Family Health Survey, (2017), only 20% women and 23% of men are covered by some form of health insurance as of 2016. More than 55% of households in India do not generally seek health care from the public sector from the lack of awareness and higher premium rates. Lack of insurance services means people with suffering from an allergy will either stop taking medical help or will choose alternate help, thereby indirectly escalating allergy prevalence in India.

Classification of allergy

Allergic classifications are made on the basis of two main triggers of allergic conditions, natural and aesthetic triggers. Although a majority of the conditions are from the natural conditions, there are aesthetic triggers that lead to allergic conditions in both adults and the children. Classification of allergy helps to understand which allergy has the most prevalence and what factors cause these allergies.

Allergy prevalence in India on the basis of classification

About 20-30% of the Indian population suffers from at least one allergic disease annually (Chandrika, 2016). In case of children, another multi-centric study found that allergic rhino-conjunctivitis occurred in 3.3% of children aged 6-7 years and 5.6% of children aged 13-14 years in India (Puri et al., 2013). Puri et al. also estimated that socio-economically the prevalence of allergies amongst the population of India comprises of 27.1% in lower class 33.3% in middle class, 28.6% in upper class in an urban area and 11.1% in the village. However, allergic rhinitis, which is the most allergy prevalence diseases in India, affects between 10% and 30% of all adults and as many as 40% of children as of 2016 (Chandrika, 2016).

On the other hand, 2.7% of young (below 15 years) and 15% of the population aged 30-50 years suffer from Eczema annually in India (Bhattacharjee et al., 2018). Furthermore, 2-3% of all patients suffering from any disease are prone to have allergic reactions such as dryness of mouth, rashes, toxicity in blood, and intolerance from drugs. Vaidyanathan et al. (2011) found that on an average 1 out of 57 patients suffering from allergic reactions due to intolerance to various drugs, mainly antibiotics. Over 15% of the total allergic population suffer from allergic reaction during winter and early winters due to seasonal change. Thus, the allergy prevalence conditions largely affect the Indian population.

Healthcare insurance in India

Insurance provides financial and economic support to patients for effective treatment. Over the years the number of medical insurances in India has increased drastically. Medical insurances are provided by both private organizations and government organizations. Eligibility of insurance in India for treatment procedures are based on health conditions, pre-existing conditions, smokers and alcoholism, family history, occupational conditions, financial stability, and other demographic factors (The Gazette of India, 2016). However, the provision of insurance in India for allergic conditions is still impoverished.

Insurance based on allergic conditions is only provided in cases of severity and life-threatening. There is no insurance policy for minor allergic reactions in India. However, severe allergic reactions like asthma, allergic rhinitis, and allergies from food are covered by a few medical insurances. These being the most common and severe allergic conditions, various insurance policies are availed to sufferers of these conditions.

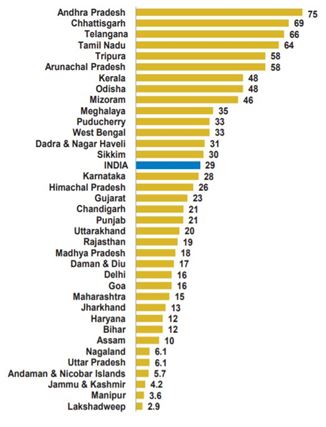

Reports of National Family Health Survey, (2017) indicated that out of India’s 135 crore population, 100 crores have no coverage against health expenses. However, according to National Health Profile, (2018), 437,457 persons were covered under health and medical insurance as of 2017, amongst them, 79% were covered by public insurance companies, with the remaining being covered by private insurance companies. Per capita, public expenditure on health in nominal terms has gone up from Rs 621 in 2009-10 to Rs 1112 in 2015-16. India spends only 1.02% of its GDP (2015-16) as public expenditure on health that also includes government health insurance schemes (National Health Profile, 2018). Around 43 crore individuals were covered under some health insurance in the year 2016-17. This amounts to 34% of the total population of India. 79% of them were covered by public insurance companies.

Overall, 80% of all persons covered with insurance fall under Government sponsored schemes which supports the below poverty level population. The percentage of households in which at least one usual member is covered by health insurance or a health scheme increased from 5% to 29% in the 10 years between NFHS-3 and NFHS-4 (National Family Health Survey, 2017). At least one usual household member is covered under any health insurance or health scheme in less than one-third (29%) of households. However, the government of India plans to improve the percentage of medical insurance by the introduction of Ayushman Bharat, a National Health Protection Scheme, which aims to cover approximately 50 crore vulnerable families (Central Bureau of Health Intelligence, 2018).

Types of health insurance available to the Indian public

In India, most of the health insurance policies are based on hospitalization, critical illnesses and medical procedures (Ministry of Health and Family Welfare, 2017). Allergic conditions with hospitalization are not yet covered by any of the private insurance policies in India. Allergic conditions are however covered in cases of critical illnesses and medical procedures. However travel health insurance plans for people travelling abroad cover treatment of allergic conditions. These plans comprise medical emergencies, evacuation, and sometimes life insurance. They, therefore, cover allergic conditions along with any health condition a person may face while travelling abroad.

Most popular medical insurances in India that cover treatment of severe allergies are:

- Max Bupa Health Insurance,

- Bharti AXA Health Insurance,

- National Health Insurance, and

- SBI Health Insurance.

Pradhan Mantri Suraksha Bima Yojana, Rashtriya Swasthya Bima Yojana, Universal Health Insurance Scheme, and Aam Aadmi Bima Yojana are some of the government insurance policies in India that cover treatment of allergies. The private insurance policies also comprise of coverage of pre-hospitalization, in-patient treatment, post-hospitalization coverage, and long term treatment procedures.

Basic regulations for the formation of health insurance policy

In India, all health insurances are based on the guidelines provided by the IRDAI (Health Insurance) Regulations as per the Section 34 (1) of Insurance Act, 1938 and under the powers vested with Regulation 2 (i) (o) (IRDAI, 2017). Insurances are provided during accidents, wherein a sudden, unforeseen and involuntary event caused by external, visible and violent means.

Insurances also cover patients with:

- A continuous period of illness and also includes relapse,

- Congenital anomaly or a condition that is present since birth,

- An acute condition including all chronic illness, that need long-term monitoring, and

However, there are several conditions where the immune system of the individual causes an overreaction to some allergens, for example, asthma, rhinitis, anaphylaxis, eczema, etc (IRDAI, 2017). Such conditions can cause severe problems and even at some point can lead to loss of consciousness or major breathing issues. The current guidelines of IRDAI are yet to emphasize in such cases.

Factors considered in designing a health insurance plan in India

Target audience as a decision factor

The target audience is the most important aspect considered by any insurance company before rolling out a medical or health insurance plan. The target audience may be a specific group of people of a specific age or gender or income or occupational category. For instance, India’s Mandatory Employee Insurance allows under the Employees’ State Insurance Act, 1948 amended by Ministry of Labour and Employment mandates compulsory health insurance to employees of low-grade income and occupation (Ministry of Labour & Employment, 2017).

The strategy of insurance marketing as a decision factor

Uniqueness or innovation in health insurance is also a market strategy that the insurance companies consider to compete in the insurance sector. For instance, the ICICI Lombard Complete Health Insurance Policy designed to protect the complete family against expenses incurred in case of hospitalization only. The policy also invites for treatments under Ayurveda, Unani, Siddha and Homeopathy (AYUSH) while hospitalized (ICICI, 2016). ICICI Lombard Complete Health Insurance Policy compete for the majority of insurance providers with the provision of treatments under AYUSH. This is contemplated by 0.8 million practitioners of AYUSH system of medicines.

Moreover, 77% of Indian households used AYUSH products in 2017, a steep rise by 69% of AYUSH households as purchased and used in 2015. In addition, a steep rise of 50% for patients seeking AYUSH treatment between 2013 and 2017 (Ministry of AYUSH, 2018). AYUSH covers almost majority of treatments starting from simplest common cold and seasonal allergic reactions to Alzheimer’s treatment. It is true that the population with allergic reactions is increasing in India, yet not as robust and steep rise to people considering AYUSH treatments (AYUSH, 2017). However, it may be considered that health insurance companies are trying to reach people with allergic conditions indirectly with the treatment of AYUSH.

Prevalence of the disease as a decision factor

Another important aspect considered by the insurance companies usually comprises of the epidemiology of the diseases, especially allergy prevalence ought for consideration for the coverage. Every insurance policy has inclusion and exclusion criteria upon which they consider the implementation of plans (Ernst & Young, 2018). In addition, epidemiology of the diseases also acts as a factor that affects health insurance premium. The lower the epidemiology of the disease or the health issue, higher is the premium of the health insurance and vice-versa (Ernst & Young, 2018). Allergy is usually acquired by birth and is considered less life-threatening. Therefore, private health insurance providers lack confidence in covering allergy related cases. However, they do consider under cases of high risk and near death experiences.

Cost and economies as a decision factor

Cost and economies play a major stake in the implementation of health policy. Insurance companies target an audience with capability on the basis of income per capita and history of prior health insurances (The Economic Times, 2014). Insurance policies have multiple premium options and objectives, effective returns and finances from the health insurance are of prime concern. For instance, Apollo Munich provides health insurances for various health issues under four different health insurance policies (Apollo Munich, 2017). However, the premium changes on the basis of age, sum insured, and years of coverage (The Economic Times, 2014). Moreover, the premium also changes on the basis of the disease and its severity. So keeping a constant premium amount reduces the target audience, while multiple low rates and high rate premiums help target a larger audience.

Availability of data and statistics as a decision factor

Lastly, data and statistics play a major role, whereby the insurance companies can forecast the feasibility of insurance with respect to audience outreach and financial returns. Ground-based data usually retrieved from hospitals and patient care units, whereby the frequency of patient visits and cost helps identify the cost estimates and expenditure and plan insurance with respect to the data (Live Mint, 2017).

Comparison of health insurance in India and the USA

The health insurance remains much more prevalent in the USA as compared to India. In India, a mere 29% of the population remain insured with some kind of healthcare plan, out of which most of the population are BPL. Whereas in the USA, over 50% of the population is covered by both public and private health insurances. The main reason behind this is that there is a lack of knowledge about the importance of health insurance in India (IRDAI, 2017). On the other hand, in India, the health insurance companies remain profit oriented and remain leaned towards the benefits of the insurer (Goel, 2016). The table below summarizes the difference between the health insurance in the USA and India that reveals the reason behind the less prevalence of health insurance in India.

S. No. |

Features |

USA |

India |

| 1. | Coverage | The insurance policies in the USA cover everything from a doctor’s visit to hospitalization for critical illness. | The health insurance in India only covers the charges of hospitalization and 30-60 days pre-post visits to the doctors. |

| 2. | Degree of compliance | It is compulsory for every individual to be covered with health insurance and also for the employers it is necessary to make sure that each of his employees is covered under medical insurance. | The insurance in India is optional. Only the people who can afford the premium of the insurance are having the benefits of it. It is also not mandatory for employers to provide health insurance for their employees. |

| 3. | Rates of premium | Per capita on health care is in the U.S. was $10,224 in 2017 and gross expenditures for healthcare stands at approximately 15% of GDP. Therefore, more people are covered under health insurance in the USA causing the premium rates are higher and the standard of living is much better. | Premium rates are lower in India because less number of people is covered in it and if the premium rates will become higher it will discourage people from taking health insurance. Impacted by poor per capita per year on healthcare at US$ 63 in 2017, and the total expenditure on healthcare 4% of GDP. |

| 4. | Health benefits provided to employees | It is mandatory to provide health insurance to every employee during their period of employment and in some cases, it gets extended till they get a new job after resignation. | In India, there is no rule that employers must provide health insurance to their employers and even if they do so it is only restricted to their duration of job period and after resignation either they have to buy the health insurance privately or get another job where the insurance is provided by the company. |

| 5. | A state-wise difference in the health insurance policy | The health insurance policies differ in each state of USA as there are different sets of rules and regulation of the health insurance policy, that are best suited for that particular state. | There is no such customization of the health insurance policy for each state. The entire country follows the same set of rules and regulations of health insurance. |

| 6. | Healthcare funding | The Government of USA provides huge expenditures with respect to healthcare and insurances. This expenditure plan also helps initiation of allergy-specific insurance policies in the USA. | The Indian Government only provides healthcare insurance expenditure to the below poverty level (BPL) population. |

Gaps in the insurance policies of India

India lacks strictness of regulations and control on medical insurance provision and control over insurance providers regarding quality, cost or data sharing makes it difficult for proper underwriting and actual premium setting. Moreover, IRDAI policy guidelines leave out many diseases that are critical to people. Allergy prevalence, one such case whereby medical insurance not provided under normal circumstances unless it’s a life-threatening case.

The USA consists of specific organizations like the Asthma and Allergy Foundation of America, that provide funds and insurance to treat allergic conditions. Such healthcare facilities are not yet available for the Indian public. Moreover, there are federal programmes which provide health insurance to the aged suffering from allergic reactions.

Lack of government funding, budgeting, and policy-making are important for the provision of healthcare insurance. Poor healthcare expenditure and per capita expenditures form another gap in the healthcare ecosystem of India. Lack of awareness and education among the rural population of India increases allergy prevalence. This adds to the burden of the economy of the country.

Impact of the pharmaceutical sector on the prevalence of allergy in India

The Indian pharmaceutical sector was valued at US$ 33 billion in 2017. The country’s pharmaceutical industry expected to expand at a CAGR of 22.4% over 2015–20 to reach US$ 55 billion. India’s pharmaceutical exports stood at US$ 17.27 billion in 2017-18 (IBEF, 2018). In 2018-19 these exports expected to cross US$ 19 billion. The drugs and pharmaceuticals sector attracted cumulative FDI inflows worth US$ 15.83 billion between April 2000 and June 2018, according to the data released by the Department of Industrial Policy and Promotion, (2018). Medicine spending in India is expected to increase at 9-12% CAGR between 2018-22 to US$ 26-30 billion, driven by increasing consumer spending, rapid urbanisation, and rising healthcare insurance (IBEF, 2018).

India continues to enjoy a prominent position in the global generic pharma space, due to many preferred advantages such as a large number of USFDA approved sites coupled with low capital expenditure and operating costs. As a result, the pharmaceuticals sector witnessed 51 pharma deals in the year 2016, with an aggregate value of USD 4.6 billion (IBEF, 2017). The growth of Indian allergic drug market is driven by epidemiological factors, affordability, accessibility, acceptability, research and development capabilities, and availability or resources (McKinsey & Company, 2018). In addition, national policies like:

- the Uniform Code of Pharma Marketing Practices and National Pharmaceutical Pricing Policy 2012,

- and international policy like USFDA’s Generic Drug User Fee Amendments (GDUFA)

are also responsible for driving the growth (Department of Pharmaceuticals, 2018).

The growth drivers of the Indian pharma industry specifically for the allergy drug market are increasing at an exponential rate. These factors also act as drivers for the management of allergic conditions in India. The allergy-related conditions are surprisingly increasing in India. The alarming rise of allergic health conditions and costs of medical care in India has caused an economic burden. However, plans to improve healthcare services like medical insurances by the Government of India, expected to reduce the economic burden and help in better management of allergic conditions in India.

Factors that impact the pharmaceutical drug market of India

It is evident that from the study that India lacks a will to manage the increasing allergy prevalence. Lack of awareness and lack of appropriate policy implementations mainly impacted and led to this conclusion. However, the Indian private pharmaceutical sector has been diligently working despite various challenges and benefiting factors in the development and growth of the allergy drug market. These factors include:

- government policies,

- drug quality,

- economic and financial stability,

- public relation,

- research and development expenditure,

- allergy prevalence and,

- research capability and resource availability.

The growth and development of the Indian pharmaceutical industry are based on these challenging and benefiting factors. Therefore, it is important to make an in-depth study of these factors to assess how these factors impact the Indian allergy drug market. Assessing the factors will help indicate the strategies that Indian pharma industries must take in order to tackle the challenges and flourish in the international market. Assessing the factors will also help understand different methods the government and pharmaceutical industry may implicate in the management of allergy prevalence in India.

References

- AYUSH. (2017). National Ayush Mission. [online] Available at: http://ayush.gov.in/sites/default/files/4197396897-Charakasamhita%20ACDP%20%20english_0.pdf

- Bhattacharjee, S. et al. (2018) ‘Prevalence and Risk Factors of Asthma and Allergy-Related Diseases among Adolescents (PERFORMANCE) study: rationale and methods’, ERJ Open Research, 4(2), pp. 00034–2018. doi: 10.1183/23120541.00034-2018.

- Bhattacharya, K. et al. (2018) ‘Spectrum of Allergens and Allergen Biology in India’, International Archives of Allergy and Immunology. doi: 10.1159/000490805.

- Central Bureau of Health Intelligence (2018) National Health Profile.

- Chandrika, D. (2016) ‘Allergic rhinitis in India: an overview’, International Journal of Otorhinolaryngology and Head and Neck Surgery, 3(1), pp. 1–6. doi: 10.18203/issn.2454-5929.ijohns20164801.

- Department of Industrial Policy and Promotion. (2018). Export Products (Pharmaceuticals). Available at: http://www.mci.gov.sa/en/Pages/Default.aspx.

- Department of Pharmaceuticals. (2018). Department of Pharmaceuticals | Government of India. Available at: http://pharmaceuticals.gov.in/ (Accessed: 16 January 2019).

- Ernst & Young. (2018). Global analysis of health insurance in India The prospects for health care in India. Available at: http://www.ey.com/Publication/vwLUAssets/EY-global-analysis-of-health-insurance-in-india/$File/ey-global-analysis-of-health-insurance-in-india.pdf.

- Goel, N. (2016). Insurance in India and the West: A comparative study. Available at: https://www.businesstoday.in/opinion/columns/money-today/naval-goel-ceo-policyx-com/story/231861.html (Accessed: 29 October 2018).

- IBEF. (2018). Indian Pharmaceutical Industry, India Brand Equity Foundation. Available at: https://www.ibef.org/industry/pharmaceutical-india.aspx.

- ICICI. (2016). AYUSH Coverage under Health Insurance. Available at: https://www.icicilombard.com/insurance-information/home-insurance-info/article/ayush-coverage-under-health-insurance (Accessed: 16 December 2018).

- Ilangovan, K. (2014). ‘Health Insurance in India: the Role of Public and Private Health Insurance Providers’, International Journal of Business and Administration Research Review, 1(6), pp. 135–137.

- IRDAI. (2017). Insurance Regulatory and Development Authority

(Health Insurance) Regulations, 2013. [online] Available at: http://ayush.gov.in/sites/default/files/Gazette%20IRDA%202013.pdf. - Livemint. (2017). Lack of adequate systems , infrastructure leading to hospital- associated infections. Available at: https://www.livemint.com/Science/O8FeBWuLKvgEKrLvvUzxKL/Lack-of-adequate-systems-infrastructure-leading-to-hospital.html (Accessed: 16 November 2018).

- McKinsey & Co. (2018). India Pharma 2020: Propelling access and acceptance, realizing true potential, McKinsey & Co.

- Ministry of AYUSH. (2018). AYUSH treatment and status in India. Available at: http://www.ayush.gov.in/ (Accessed: 26 December 2018).

- Ministry of Health and Family Welfare. (2017). National Family Health Survey (NFHS-4). doi: 10.1016/S0140-6736(05)17806-4.

- Ministry of Labour & Employment. (2017). Insurance for labourers and skilled labourers. Available at: https://labour.gov.in/ (Accessed: 28 December 2018).

- National Family Health Survey. (2017). National Family Health findinsg and hralth profile. doi: 10.1016/S0140-6736(05)17806-4.

- National Health Profile. (2018). National Health Profile (NHP) of India- 2018. Available at: https://www.cbhidghs.nic.in/index1.php?lang=1&level=2&sublinkid=88&lid=1138.

- Puri, S. (2013). ‘Pattern and Distribution of Ocular Morbidity in Patients Visiting the Field Practice Area of Tertiary Care Hospital of North India’, Journal of Biomedical and Pharmaceutical Research, 2(2), pp. 42–46. Available at: jbpr.in/index.php/.

- The Economic Times. (2014). Insurance: Know how premium, cover and term changes with your age and marital status. Available at: https://economictimes.indiatimes.com/wealth/insure/insurance-know-how-premium-cover-and-term-changes-with-your-age-and-marital-status/articlesh? (Accessed: 16 November 2018).

- The Gazette of India. (2016). ‘Insurance Regulatory and Development Authority of India-Guidelines’. Hyderabad. Available at: https://www.irdai.gov.in/ADMINCMS/cms/frmGeneral_Layout.aspx?page=PageNo61&flag=1.

- Vaidyanathan, S. (2011). ‘Nasal AMP and histamine challenge within and outside the pollen season in patients with seasonal allergic rhinitis’, Journal of Allergy and Clinical Immunology, 127(1). doi: 10.1016/j.jaci.2010.09.006.

Discuss