Activity-based costing or ABC model in logistics

The Activity-based Costing (ABC) model is one of the many approaches to estimate logistics costs. The term was coined in the late 1980s by Robert Cooper and Robert Kaplan in their article titled, “Measure Costs Right: Make the Right Decisions.” ABC model is defined as a management accounting technique which allocates costs to different activities that consume organizational resources thereby identifying the costs per product or service or customer (Themido et al., 2000). Conventionally, logistics costs were determined as a gross figure, but later on, it was realized that such measures usually present a fallacious account of the logistics costs. This is because logistics functions take place in a dynamic environment.

Shortcomings of traditional methods of estimating logistics cost

Cooper and Kaplan argued that traditional supply chains were uncomplicated because businesses produced lesser products and transferred these to the consumers through simple marketing channels. Over time, the businesses started producing multiple products and the distribution channels also proliferated. The result was that the share of direct costs in total logistics costs were reduced and the indirect costs captured the major part. Thus, the need for a new cost accounting tool was realized. The following figure highlights the average costs for the essential elements of logistics costs as a percentage of sales.

An example to illustrate the ABC model

Two watch manufacturers (A and B), both produce 10,000 units every year. While manufacturer A deals in a single product i.e., men’s watches, manufacturer B deals in men, women, and kids watches. Traditional costing systems would simply calculate the costing of both businesses by aggregating total output and dividing it by total manufacturing costs. In this case, manufacturer B would never be able to know which of the three items it produces consumes maximum costs and generates the least revenue. In contrast, the ABC system would allocate output and costs into the activities that took place while producing these items. The ABC system can thus present the costing per product even when the business produces multiple products which were not possible with the conventional approach.

How ABC is different from others?

The underpinning postulation of logistics costing is to recognize the various costs involved by selling a set of assorted market offerings to the customers. Conventionally, there were two accounting methods widely adopted:

- Direct Product Profitability (DPP) and,

- Customer Profitability Analysis (CPA).

DPP method of estimating logistics cost

DPP method is a volume-based method wherein direct and indirect costs were allocated as per volume (Fernie, Freathy and Tan, 2001). It is the most widely adopted technique. It involves taking all the costs involved with a product from production to point of sales. It is more relevant for retail products as it serves a profitability parameter. Here marketers can assess the gross profit by considering factors like manufacturing costs, warranties, financial overheads, storage, and handling, minus the total sales. The method is useful for gauging the lucrativeness of the product under consideration with respect to profit. Retailers and distributors tend to stock up products with high DPP and discard the ones with lower DPP. Thus, making the scope for the introduction of new products. Therefore, stock-keeping units can be optimized and also better pricing and promotions strategies can be designed (Themido et al., 2000; Bookbinder and Zarour, 2001).

CPA method of estimating logistics cost

On the other hand, CPA denotes working out the actual cost a business incurs to serve an individual customer. It helps businesses to calculate the net profit generated from each customer (Sales-costs). The costs encompass not only production and distribution costs but also sales, marketing, customer services and any other costs. Cost allocation is done while considering the marginal cost which may not incur if the customer is not served. Based on the determined profitability per customer, the customers can be categorized into tiers ranging from unprofitable or undesired to most profitable.

CPA is extensively used by banks to sell credit cards. The highest perks and services are offered to the top two tiers and even attempt to bring tier-three customers to the top two tiers (Raaij, Vernooij, and Triest, 2003; Raaij, 2005). The biggest challenge of this method is to calculate the cost accurately. Particularly for services wherein time and efforts expended varies from customer to customer. Moreover, the cost of lost customers needs to be considered. If ignored, may reflect customers to be more profitable than they actually are (Guerreiro, Rodrigues Bio, and Vazquez Villamor Merschmann, 2008). Furthermore, conventional accounting systems are incompetent to provide suitable information for this methodology (Themido et al., 2000).

ABC model of estimating logistics cost

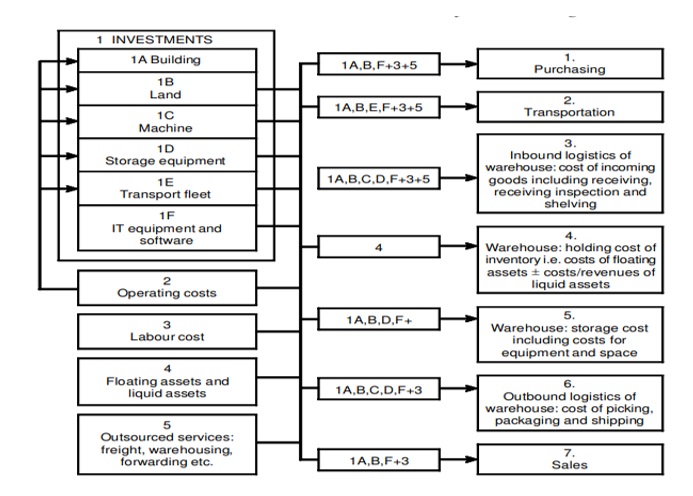

The ABC Model is an improvisation of both DPP and CPA methods. It is a recently evolved method and discounts the conventional cost accounting practices. It aims to list out the activities that utilize any factor of production. Therefore, generating a cost flow assignment chain that helps the easy allocation of costs. It helps in the classification of the cost drivers through the value chain and allocates the subsequent cost to the cost center. Hence, it more accurate as it reflects true cost or true profitability against the conventional methods based on gross profit margins. A better understanding of the return on investment (ROI) can be thus, expected. It also helps to better filter the direct and indirect costs, thereby, correcting the costing fallacies of the traditional methods. The only drawback of the ABC method is that it is laborious for its intense data requirements (Schmidt, 2019).

Application of ABC in real-time practices

Based on the analysis of the ABC system, it is wise to see how much it is being used in the real-world scenario. Arora & Raju (2018) explored the large and medium scale Indian manufacturing units with at least 100 employees and plant and machinery worth Rs. Five crores or more. Through the empirical study, it was found that the ABC model offered benefits like:

- result-oriented pricing tactics,

- better cost and overhead allocation and,

- accurate assessment of product cost.

However, the challenges were the identification of the cost drivers, impending cost of implementing the ABC system, glitches of data assimilation and ambiguity. Thus, many businesses are still adamant to use conventional cost accounting methods. Similar findings were registered by Nair & Tan (2018) who conducted a primary study amongst 200 financial executives working in Malaysian small and medium scale businesses. Not many of them have implemented the ABC method due to the perception of it being expensive.

Chrysler’s use of the ABC model in logistics

On the positive side, Chrysler implemented the ABC system in 1991. Overcoming the aforesaid hurdles of implementation, ABC helped in radical organizational learning and team building through a redesigned financial system. The personal contribution was encouraged through change agents which eventually streamlined everything at the auto giant in five years. As a result, product designs were simplified and wasteful and ineffective activities were eradicated. It culminated into the savings being 50-100 times more than the implementation cost (Meador, 2018). Likewise, Safety-Kleen, a waste recycling midsize entity, have registered a savings of over 13 million USD through better revenues and cost pruning. It is nearly 14 times what has been invested in the system. The outcome was facilitated by discarding loss-making offerings, downsizing of operations and entering new markets (Ness and Cucuzza, 1991).

References

- Arora, A. K. and Raju, M. S. S. (2018) ‘An analysis of activity based costing practices in selected manufacturing units in India’, Indian Journal of Finance. Associated Management Consultants Pvt. Ltd., 12(12), pp. 22–31. doi: 10.17010/ijf/2018/v12i12/139889.

- Bookbinder, J. H. and Zarour, F. H. (2001) ‘DIRECT PRODUCT PROFITABILITY AND RETAIL SHELF-SPACE ALLOCATION MODELS’, Journal of Business Logistics. Wiley, 22(2), pp. 183–208. doi: 10.1002/j.2158-1592.2001.tb00010.x.

- Fernie, J., Freathy, P. and Tan, E.-L. (2001) ‘Logistics Costing Techniques and their Application to a Singaporean Wholesaler’, International Journal of Logistics Research and Applications. Informa UK Limited, 4(1), pp. 117–131. doi: 10.1080/13675560110038103.

- Guerreiro, R., Rodrigues Bio, S. and Vazquez Villamor Merschmann, E. (2008) ‘Cost-to-serve measurement and customer profitability analysis’, The International Journal of Logistics Management, 19(3), pp. 389–407. doi: 10.1108/09574090810919215.

- Manunen, O. (2000) ‘An Activity-Based Costing Model for Logistics Operations of Manufacturers and Wholesalers’, International Journal of Logistics Research and Applications. Informa UK Limited, 3(1), pp. 53–65. doi: 10.1080/13675560050006673.

- Meador, D. (2018) The Systems Thinker – ABC: Initiating Large-Scale Change at Chrysler – The Systems Thinker, Systems Thinker.

- Nair, S. and Tan, X. (2018) ‘Factors Influencing the Implementation of Activity-Based Costing: A Study on Malaysian SMEs’, International Business Research. Canadian Center of Science and Education, 11(8), p. 133. doi: 10.5539/ibr.v11n8p133.

- Ness, J. and Cucuzza, T. (1991) Tapping the Full Potential of ABC, Harvard Business Publishing.

- Raaij, E. M. (2005) ‘The strategic value of customer profitability analysis’, Marketing Intelligence and Planning, 23(4), pp. 372–381. doi: 10.1108/02634500510603474.

- Raaij, E. M., Vernooij, M. J. A. and Triest, S. (2003) ‘The implementation of customer profitability analysis: A case study’, Industrial Marketing Management, 32(7), pp. 573–583. doi: 10.1016/S0019-8501(03)00006-3.

- Schmidt, M. (2019) Is Activity Based Costing Worth the Extra Time and Effort?, Captain’s Log.

- Themido, I. et al. (2000) ‘Logistic costs case study—an ABC approach’, Journal of the Operational Research Society. Taylor & Francis, 51(10), pp. 1148–1157. doi: 10.1057/palgrave.jors.2601031.

I am a management graduate with specialisation in Marketing and Finance. I have over 12 years' experience in research and analysis. This includes fundamental and applied research in the domains of management and social sciences. I am well versed with academic research principles. Over the years i have developed a mastery in different types of data analysis on different applications like SPSS, Amos, and NVIVO. My expertise lies in inferring the findings and creating actionable strategies based on them.

Over the past decade I have also built a profile as a researcher on Project Guru's Knowledge Tank division. I have penned over 200 articles that have earned me 400+ citations so far. My Google Scholar profile can be accessed here.

I now consult university faculty through Faculty Development Programs (FDPs) on the latest developments in the field of research. I also guide individual researchers on how they can commercialise their inventions or research findings. Other developments im actively involved in at Project Guru include strengthening the "Publish" division as a bridge between industry and academia by bringing together experienced research persons, learners, and practitioners to collaboratively work on a common goal.

Discuss